Vermont’s FY2027 Budget: $9.3 Billion in Spending, Built on Money That Won’t Be There Next Year

The House approved a spending plan nearly identical to the governor’s — but the fight over property taxes, one-time revenue, and who pays for what is just getting started.

The Vermont House Appropriations Committee voted unanimously on Monday to send its FY2027 budget bill, H.951, to the full House floor. The $9.334 billion spending plan covers July 2026 through June 2027 and is roughly $1 million less than Gov. Phil Scott’s $9.335 billion proposal from January.

On the surface, this looks like broad agreement. The House and the governor are a million dollars apart on a $9.3 billion budget. That’s a rounding error.

But the real story isn’t the spending total. It’s what’s underneath it — where the money comes from, how long it lasts, and what happens to your property tax bill as a result.

The property tax question nobody’s connecting to the budget

Back in December, the state Tax Department projected that education property taxes would spike by roughly 12% in the coming year. Both the governor and the House agree that’s unacceptable, and both want to use about $105 million in one-time money to bring it down.

That’s where the agreement ends.

Gov. Scott wants to spend the full $105 million this year, which his administration estimates would hold the average increase to around 4%. The House Ways and Means Committee — on a close 6-5 vote, largely along party lines — chose a different path. The yield bill, H.949, would spend roughly half the $105 million (~$52.45 million) plus the estimated FY2026 Education Fund surplus (~$22.3 million) this year, producing an estimated average increase of about 7%. The remaining ~$52.45 million would be reserved to help offset property tax increases in FY2028.

The logic: if you spend all the one-time money now, next year you’d face an even larger spike with nothing left to cushion it. The counterargument: Vermonters need relief now, not a promise of partial relief spread over two years.

The governor has already pushed back. In his State of the State address, he threatened to veto the budget if legislators don’t advance the education reforms in Act 73, the sweeping education law passed last year at his administration’s urging.

This distinction — 4% vs. 7%, all now vs. spread over two years — is arguably the most consequential fiscal decision of the session for Vermont homeowners. Most coverage of the budget has treated the spending bill and the yield bill as separate stories. They’re not. They’re companion legislation, and understanding one without the other leaves out the piece that matters most to taxpayers.

What’s in the budget bill itself

The budget bill, H.951, adds $17.5 million in General Fund spending above what the governor proposed. But the overall budget is actually $1 million less than Scott’s plan — meaning the House is spending more in some areas and less in others. The new spending was drawn from roughly $250 million in funding requests the committee received, meaning about 93% of what agencies, legislators, and advocates asked for didn’t make the cut.

The additions include:

Six new state positions, including a mediator at the Vermont Labor Relations Board (to fill a gap left by federal cuts to the National Labor Relations Board), an attorney for the Vermont State Ethics Commission focused on municipal ethics cases the commission has said it can’t currently handle, and a position at the Vermont Human Rights Commission. The governor proposed no new positions.

A Vermont Legal Aid attorney focused on immigration cases.

A $2.7 million increase in rates paid to organizations providing mental health care and other human services, including home-based care. That state spending draws a $3.7 million federal match — meaning $6.4 million total goes to providers.

$2.3 million for expanded college tuition grants for low-income students through the Vermont Student Assistance Corporation.

Rep. Robin Scheu, D-Middlebury, who chairs the Appropriations Committee, described the committee’s approach as trying to minimize harm within a limited budget.

Where the money comes from — and why it matters

To partially fund its new spending, the House identified two revenue sources the governor did not tap:

$9.5 million in accumulated interest from a state fund set up to pay for IT infrastructure upgrades. This is money that has been sitting in the fund earning interest over several years. It’s available once.

Revenue from changing Vermont’s tax code in response to the new federal tax law (the “One Big, Beautiful Bill Act,” or OBBA, formally H.R. 1, signed by President Trump in July 2025). This is where it gets complicated — and where existing coverage has been imprecise.

Early reporting on the budget described this revenue as “about $9.4 million.” According to the Joint Fiscal Office’s fiscal note for H.933 — the tax bill that contains these changes — the gross revenue from federal tax conformity provisions is actually $15.6 million to the General Fund in FY2027.

But even the $15.6 million figure doesn’t tell the whole story, because H.933 does much more than conform to federal tax law.

The tax bill is a plumbing job, not a windfall

H.933, the miscellaneous tax bill heading to the House floor this week, reshuffles revenue between Vermont’s three major funds — the General Fund, the Education Fund, and the Transportation Fund — in ways that largely offset each other. Think of it as fiscal plumbing: reconnecting pipes between three tanks so each gets a different flow of money.

Here’s what’s actually happening, step by step:

Step 1: Federal tax conformity brings in $15.6 million to the General Fund. When Congress changed federal tax law last year, it automatically affected what Vermont taxpayers owe the state, because Vermont’s income tax is linked to the federal code. The Legislature is choosing to accept some of those changes (”linking”) and reject others (”decoupling”).

The single largest revenue gain — $19.22 million — comes from Vermont rejecting a federal deduction that lets corporations reduce their taxes on income derived from overseas operations. Vermont is choosing not to give that break at the state level. Other provisions the state links to (like changes to business interest deductions and depreciation rules) cost revenue, bringing the net to $15.6 million.

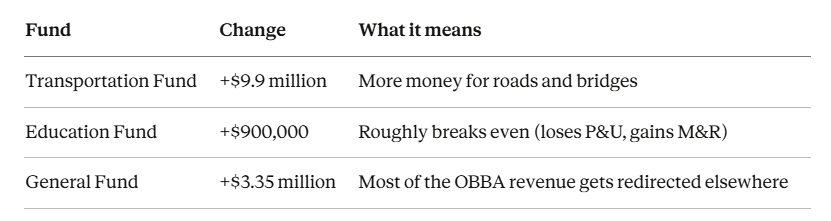

Step 2: The House shifts $10.8 million in Meals and Rooms tax revenue from the General Fund to the Education Fund. Currently, 69% of meals and rooms tax revenue goes to the General Fund and 25% to the Education Fund (with 6% to the Clean Water Fund). H.933 changes that to 65%/29%. That’s $10.8 million moving out of the General Fund and into the Education Fund.

Why? To backfill what the Education Fund loses in Step 3.

Step 3: The House shifts $9.9 million in vehicle Purchase and Use tax revenue from the Education Fund to the Transportation Fund. Currently, the split is 66.7% Transportation, 33.3% Education. H.933 changes it to 73%/27%. This is a compromise with Gov. Scott’s proposal to eventually send 100% of P&U tax revenue to the Transportation Fund to help close a projected funding shortfall for roads and bridges. The House version keeps some flowing to schools.

The net result across all three funds in FY2027:

The General Fund — the fund that pays for the new positions, the legal aid attorney, human services, and most of what the state does day-to-day — nets $3.35 million from the entire tax bill in FY2027.

One more detail worth knowing: across FY2026 and FY2027 combined, H.933’s net impact on the General Fund is negative $610,000. The bill actually costs the General Fund money in the short run because the retroactive conformity provisions create a $3.96 million revenue hit in the current fiscal year before the gains kick in next year.

So how does the House cover $17.5 million in new spending?

This is a fair question, and the answer involves the full budget picture — not just the tax bill.

The $9.5 million in IT fund interest is straightforward new money. The tax bill (H.933) provides a net $3.35 million to the General Fund. That’s roughly $12.85 million in new revenue. But the House budget is actually $1 million less than the governor’s overall, which means the committee also trimmed or reallocated spending elsewhere in the budget to make room for its priorities. The specific reductions haven’t been itemized in public coverage, and are embedded in the line-by-line budget document itself.

What we can say: the House isn’t deficit-spending. It’s making different choices about where the same pile of money goes. Some of those choices add spending (new positions, provider rates, tuition grants). Others presumably reduce it. The net is $1 million below the governor’s plan.

The structural problem underneath all of this

All of this — the budget, the yield bill, the tax bill — is a one-year fix for a multi-year problem.

The $9.5 million in IT fund interest is one-time money. The $75 million of surplus revenue being used for the property tax buydown is one-time money. The OBBA conformity revenue ($15.6 million) is technically recurring, but it depends on the federal tax law remaining unchanged — and federal tax provisions have a history of being modified, extended, or reversed.

The deeper math is sobering. Education costs in Vermont are growing at roughly 6% per year. The non-property-tax revenues that flow into the Education Fund — primarily sales and use taxes — grow at around 3%. That gap compounds every year. According to analysis in the Times Argus, roughly 80% of education spending goes to salaries and benefits, and health care premiums for school employees have increased 125% between FY2018 and FY2025. Meanwhile, K-12 enrollment has declined from roughly 98,000 students two decades ago to around 73,000 today, meaning the cost per pupil keeps climbing even as total enrollment falls.

As that same Times Argus analysis noted, holding property tax growth to even 5% per year over the next three fiscal years would require roughly $500 million in new non-property-tax revenue. This year’s buydown — whether it’s the governor’s full $105 million or the House’s ~$52 million — barely dents that trajectory.

There is also the question of federal funding. Vermont’s budget relies heavily on federal dollars — particularly Medicaid, which funds a large share of the state’s health and human services spending. Proposed federal cuts to Medicaid and other programs could force sudden, significant state budget reductions. The House budget sets aside $30 million as a reserve against potential federal cuts, but the scale of what’s been proposed in Washington could dwarf that reserve.

What to watch next

The full House is expected to vote on H.951 (the budget) and H.933 (the tax bill) this week. Both then go to the Senate, where further changes are likely.

The key questions for the rest of the session:

Will the governor accept a 7% property tax increase? He’s said he won’t. If the House and Senate hold firm on the two-year approach and the governor vetoes, the Legislature would need a two-thirds majority to override.

Will the Senate change the revenue formula? The fund-shifting in H.933 is a delicate balance. If Senate Finance adjusts any piece — the Meals and Rooms allocation, the Purchase and Use split, or the federal conformity choices — it ripples through all three funds.

What happens with education governance reform? The governor has tied his budget support to progress on Act 73 implementation. If education reform stalls, the budget itself could be at risk regardless of what’s in it.

How real is the federal funding risk? The $30 million reserve is a hedge, not a solution. If Congress follows through on proposed cuts to Medicaid and other programs, Vermont’s next budget could look very different from this one.

Note on sourcing: This analysis draws on the JFO fiscal note for H.933, the FY2027 Budget Summary from JFO, Campaign for Vermont’s review of H.949, Vermont Public’s coverage of the yield bill vote, coverage of the vehicle purchase tax changes and the governor’s State of the State address, and the “Boots on the Ground” column from the Times Argus/Rutland Herald. Where figures in news coverage conflicted with primary source documents, this article follows the primary source.

Revenue note: Early coverage of the budget described revenue from federal tax conformity changes as “about $9.4 million.” The Joint Fiscal Office fiscal note for H.933 states the gross figure is $15.6 million to the General Fund in FY2027. After fund rebalancing provisions in the same bill, the net General Fund impact is $3.35 million. We could not determine the basis for the $9.4 million figure from available primary sources.