Right or Wrong, Polymarket Is Betting on Vermont

Federal rules block Vermonters from Polymarket. The platform lists the wrong candidates in Vermont's race. Vermont's ban bill has sat untouched in House committee for eleven weeks. The bets keep going

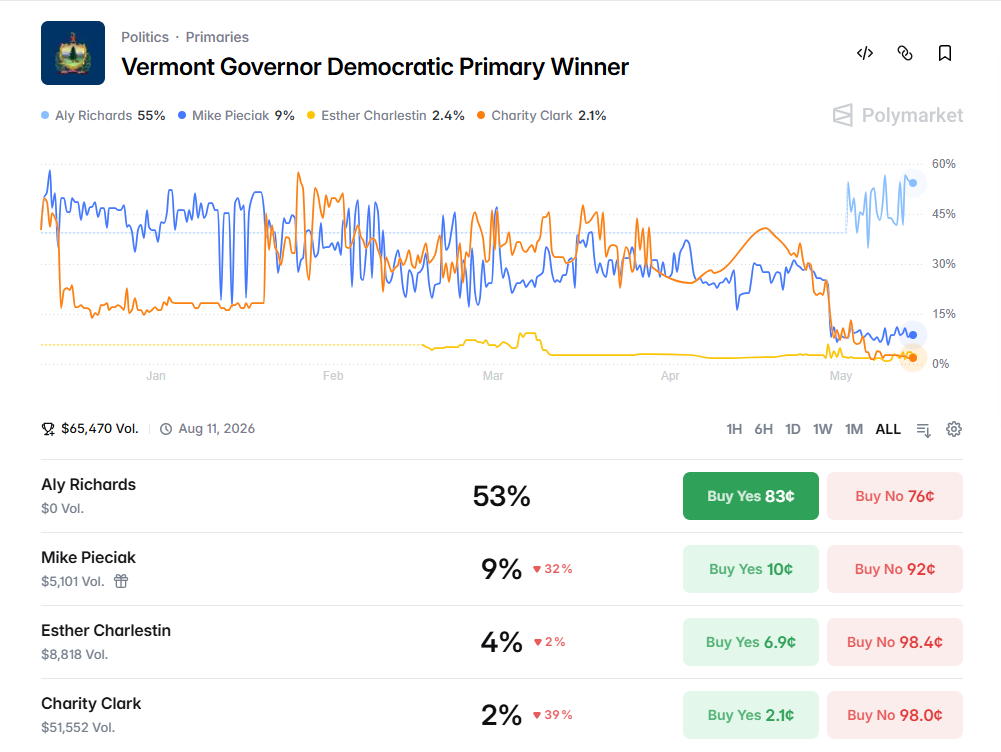

On Polymarket today, Phil Scott is priced at a 95% chance to win the Republican gubernatorial primary on August 11. Aly Richards leads the Democratic field at 57%. The Republican line sits at 78% to win the November general election. The site lists three active markets on Vermont’s 2026 governor’s race, with a combined trading volume of roughly $89,000.

None of those prices was set by a Vermonter.

Polymarket’s international platform — the one where these three Vermont markets live — geofences U.S. users out. The site’s own metadata flags both primary markets as ineligible for U.S. trading. A separate entity, Polymarket US, is operated by QCX LLC, a CFTC-regulated designated contract market that Polymarket acquired in 2025. That entity is currently in invitation-only beta and lists only sports contracts. As of today, no Vermonter can legally trade on the Vermont governor race on either platform.

The contracts are still being priced. They will continue to be priced through the August 11 primary and through November 3. The bettors who set the price are everywhere except here.

That’s the structural fact worth understanding alongside H.913, the short-form bill Rep. Tom Stevens (D-Waterbury) introduced on February 25 to criminalize political prediction-market contracts in Vermont. The bill was referred to the House Committee on Government Operations and Military Affairs the same day. It has had no recorded committee action in the eleven weeks since, and with the biennium nearing adjournment, no realistic procedural path forward this session.

Stevens’s bill treats betting on Vermont elections as a Vermont problem to legislate. The premise rests on the assumption that Vermont’s gambling regulations have something local to act on. They don’t. The behavior the bill targets is already not happening here, because federal regulatory geometry — not Vermont law — has made it impossible for Vermonters to participate.

H.913 is dying in committee. The market is running anyway.

What the market thinks it knows

The bigger problem with treating Polymarket as a source of insight into Vermont politics — which national outlets increasingly do — is that the platform’s curators have made editorial choices that don’t reflect the actual race.

Polymarket is not user-generated. The company’s own help center states plainly that “users cannot directly create their own markets,” though users can suggest ideas through Discord or social media. Polymarket’s internal team decides what events get listed and which candidates appear as outcomes. Industry reporting on emerging competitors describes Polymarket’s model as closer to Netflix than YouTube — the platform, not the user base, picks what’s on offer.

For the Vermont Democratic primary, Polymarket’s team picked four candidates on December 11, 2025: Attorney General Charity Clark, State Treasurer Mike Pieciak, 2024 Democratic gubernatorial nominee Esther Charlestin, and Aly Richards. None of those choices has aged well.

Clark announced on May 4 that she is running for re-election as attorney general, not governor. Pieciak has not announced any 2026 race. Charlestin announced in January that she is running for lieutenant governor. That leaves Richards — the listed candidate at 57% — with no actual challenger in the contract slate. And yet Polymarket has not added Amanda Janoo, who declared her candidacy on March 10 and will appear on the August ballot.

If Janoo wins the primary, the market has no clean way to resolve. Her name doesn’t exist as an outcome the contract can pay out on.

On the Republican side, Polymarket has Lieutenant Governor John Rodgers listed at 5% in the gubernatorial primary. Rodgers announced his re-election bid on February 3 — for lieutenant governor. He is not on the August ballot for the office Polymarket has him listed for. Governor Scott himself has not formally announced a re-election bid, though his campaign has been circulating petitions since early April ahead of the May 28 filing deadline.

The trading data is equally instructive. Of the $65,470 in volume on the Democratic primary market, roughly $51,500 — about 79% — was placed on Clark, who never entered the race. Another $5,101 was wagered on Pieciak. The current Democratic favorite, Richards, has zero recorded trading volume on her contract; her 57% implied probability comes from automated bid-ask spreads, not from anyone putting money behind her. On the Republican primary market, Rodgers has more trading volume ($1,714) than the incumbent governor projected to win at 95% ($1,278).

In short: the bettors most active in these markets spent most of their money on people who aren’t running.

Why this matters anyway

The natural response is to dismiss thinly-traded prediction markets that miss the basic facts. Vermont’s race is small. Total volume across all three markets is less than what a single national political market can clear in an hour. The signal-to-noise ratio is poor.

But the prices still appear in national coverage, in punditry, and in screenshots circulated on social media. A 95% reading on Phil Scott’s re-election, broadcast through the architecture of what Polymarket calls “the world’s largest prediction market,” carries narrative weight regardless of how few traders set it. And the people most affected by that narrative — Vermonters — have no mechanism to correct it from inside, because they cannot enter the market.

H.913 would do what Stevens’s bill proposes: criminalize the contracts on the books. But that’s a regulatory action against a behavior Vermont’s residents are already excluded from. It does nothing about the market itself, which exists on platforms outside Vermont’s jurisdiction, listed by a company that has decided Vermont’s race is worth pricing, with a candidate slate it doesn’t appear to maintain against reality.

The state’s authority ends at its borders. The market’s reach doesn’t.

Editor’s note, May 14, 2026: Compass Vermont emailed Rep. Tom Stevens on May 12, ahead of this piece’s publication, with detailed questions about H.913 in light of the federal regulatory issues described above. Stevens did not respond before publication on May 13. On the morning of May 14, he sent a response offering three clarifications, which Compass Vermont has independently verified and adds here.

Scope. H.913 applies more broadly than this piece described. As drafted, the bill covers prediction-market contracts on sports, contests, natural persons, politics and campaigns, disasters, war, all-hazards, or death. This article focused on the gubernatorial contracts on Polymarket, which fall under one of those seven categories.

Mechanism. H.913 includes both criminal and civil provisions. In addition to amending Vermont’s criminal statutes governing wagering, the bill would amend state contract law to render prediction-market agreements void and allow civil recovery of lost funds. Stevens describes the contract-law route as deliberately designed around federal preemption — declaring such contracts unenforceable in Vermont where the state lacks authority to criminally enforce a ban on what federal law treats as a commodity. This piece described the bill as a criminalization measure; that description is incomplete.

Committee record. The Vermont legislature’s official bill-status page for H.913 shows no formal committee action after the bill’s February 25 referral. Stevens states that the House Committee on Government Operations and Military Affairs took testimony on H.913 and H.133 on April 14, with the understanding that neither bill would advance this biennium. The bill-status page logs formal procedural actions and does not necessarily reflect hearings or testimony. This piece relied on the status page and did not separately check committee schedules.

Stevens also notes that the federal Commodity Futures Trading Commission has been operating with reduced commissioner capacity and, in April 2026, sued Arizona, Connecticut, and Illinois over their efforts to regulate prediction markets — limiting the federal consumer-protection actions available and constraining the legal space within which state action can operate. He frames H.913 as Vermont’s attempt to respond within that narrow space.

The broader analysis in this piece — that Polymarket has selected the wrong candidates in Vermont’s 2026 governor’s race, that Vermonters cannot legally trade these markets, and that the market exists and operates regardless of state action — is unchanged by these clarifications.

Rather amazing how Gambling has taken over our Society.... Mental health issue?? You bet....

Ban poly market in Vermont